1. AI Trading Is Not About “Prediction”—It’s First About “Surviving to Trade Another Day”

In trading, profit is the result, but whether your account can withstand volatility is the prerequisite. If a strategy blows up in an extreme market or suffers such a heavy loss that recovery is nearly impossible, then no matter how impressive past backtests were, they are meaningless.

Therefore, the focus of risk management is not “never losing money,” but:

- Being able to keep trading after losses

- Avoiding total loss in a single incident

- Having the ability to adjust and recover when issues arise

Mature trading systems generally share several principles:

- Small losses are acceptable; catastrophic losses are not

- Market volatility can be tolerated, but must not spiral out of control

- Control risk first, then consider increasing returns

2. Four Core Risks: Model, Market, Execution, Governance

1) Model Risk

Common risks for AI models include:

- Overfitting: Learning historical noise instead of stable patterns

- Drift: Old parameters become invalid as market mechanisms change

- Label distortion: Training objectives differ from actual trading goals

Model risk is characterized by “hard to detect in backtesting, rapid amplification in live trading.” Therefore, once a model is deployed, ongoing monitoring of signal distribution, hit rates, and return structure is essential.

(Methods for managing model risk were discussed earlier in Lesson 2, Section 4 and won’t be repeated here.)

2) Market Risk

The high volatility and strong sentiment in crypto markets make market risk more sudden:

- Rapid trend reversals

- Instant drops in liquidity

- Crowded leverage triggering cascading liquidations

These risks cannot be fully predicted by models and can only be mitigated through position sizing and scenario planning.

3) Execution Risk

Many strategies “work on paper but fail in reality” due to execution issues:

- Slippage exceeding expectations

- Incomplete order fills

- Interface delays or brief outages

- Order behavior distortion during abnormal market conditions

Execution risk directly affects actual returns and must be modeled and monitored separately—it cannot be assumed negligible.

4) Governance Risk

As system scale grows, governance issues become a hidden source of risk:

- Parameter updates without approval

- Position conflicts between multiple strategies

- No ability to roll back versions

- Unclear responsibilities during anomalies

Governance risk doesn’t immediately show as price volatility but will amplify all technical risks under stress.

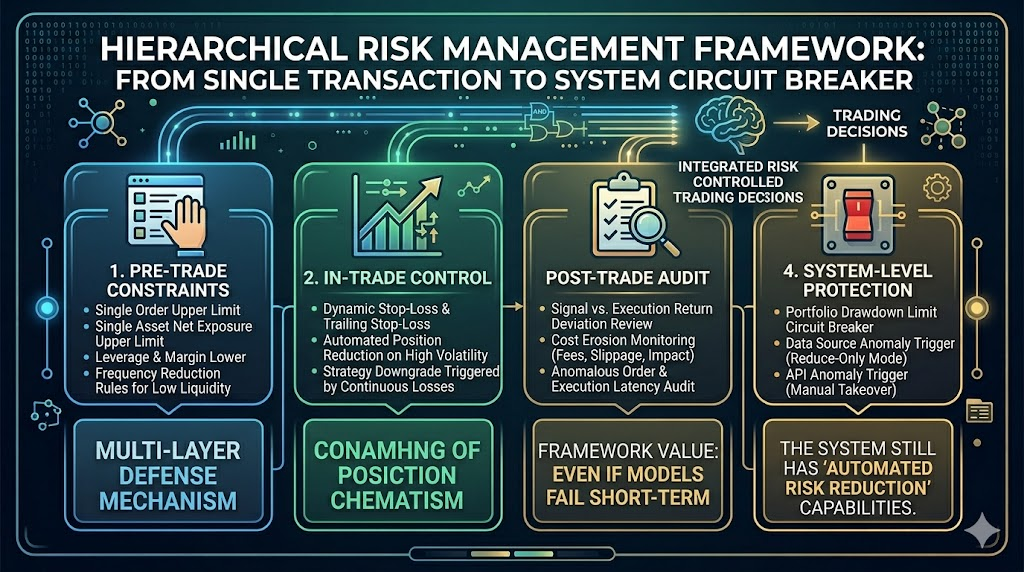

3. Layered Risk Control Framework: From Single-Trade Limits to System Circuit Breakers

Sustainable risk control typically uses a “four-layer defense”:

1. Pre-trade Constraints

- Order size limits per trade

- Net exposure limits per instrument

- Leverage and margin minimums

- Reduced trading frequency during low-liquidity periods

2. In-trade Controls

- Dynamic and trailing stop-losses

- Automatic position reduction during increased volatility

- Strategy downgrades triggered by consecutive losses

3. Post-trade Checks

- Reviewing signal vs. actual return discrepancies

- Monitoring cost erosion (fees, slippage, market impact)

- Auditing abnormal orders and execution delays

4. System-level Protections

- Portfolio drawdown circuit breakers

- Reducing positions automatically on data source anomalies

- Manual intervention triggered by interface issues

- Automatic risk reduction during major event windows

The value of this framework is that even if the model fails in the short term, the system still has “automatic risk reduction capability.”

4. Risk Budgeting: Writing “Acceptable Losses” Into System Rules

Many strategies fail not due to wrong direction but due to mismatched positions and volatility.

A risk budgeting mechanism answers three questions:

- What’s the maximum drawdown a single strategy can bear?

- What’s the maximum daily loss threshold?

- How should risk quotas be allocated across multiple strategies?

In practice, use a dual constraint of “volatility normalization + drawdown thresholds”:

- Automatically reduce nominal positions as volatility rises

- Force lower trading frequency or pause when drawdown thresholds are hit

This prevents using position templates suited for low-volatility periods during high-noise phases.

5. Stress Testing: Validating System Boundaries in “Worst-case Scenarios”

Standard backtests only cover “what has happened,” but risk control must focus on “potential extreme states.”

Stress tests should at least cover these scenarios:

- Sudden large gaps (no continuous trading intervals)

- Sharp drops in order book depth (nonlinear rise in slippage)

- Data delays or interruptions (signal-market decoupling)

- Surging cross-asset correlations (portfolio diversification failure)

The goal of stress testing is not to predict when extreme events will happen but to verify whether the system can still exit controllably under extreme conditions.

6. Monitoring and Alerts: From “Post-event Review” to “Real-time Intervention”

The key to mature risk control is real-time monitoring.

Recommended metrics fall into three categories:

- Strategy health indicators: hit rate, profit/loss ratio, signal trigger frequency

- Execution quality indicators: slippage deviation, fill rate, latency distribution

- System stability indicators: data integrity, API availability, number of risk triggers

Alert mechanisms should have tiers:

- Level 1 Alert: For observation only

- Level 2 Alert: Automatic position reduction

- Level 3 Alert: Strategy pause with manual intervention required

This structure prevents the system from “losing control all at once” as risks accumulate.

7. Integration with Automated Infrastructure: Engineering Risk Management

As the number of strategies increases, manually maintaining risk rules quickly becomes unmanageable.

At this stage, platform capabilities (such as infrastructure like Gate for AI) matter for risk control by:

- Standardizing rules: Unified risk thresholds and trigger logic

- Centralizing monitoring: Strategy, execution, and system metrics on a single dashboard

- Automating responses: Quick execution of position reduction, limits, or shutdown after a trigger event

It’s important to note that tools improve risk control efficiency; boundaries themselves must still be defined by the strategy governance framework.

8. Lesson Summary

The success or failure of AI trading systems depends on risk management—not prediction accuracy. Models will fail, markets will shift suddenly, executions will deviate, governance can break down; only with layered risk controls and real-time monitoring can systems survive long term. In the next lesson, we’ll focus on why intelligent trading must move toward human-machine collaboration, how to build a sustainable strategy operations framework, and which capabilities will define future competitiveness.