I. From Forwards to Futures: The Most Basic Price-Locking Tool

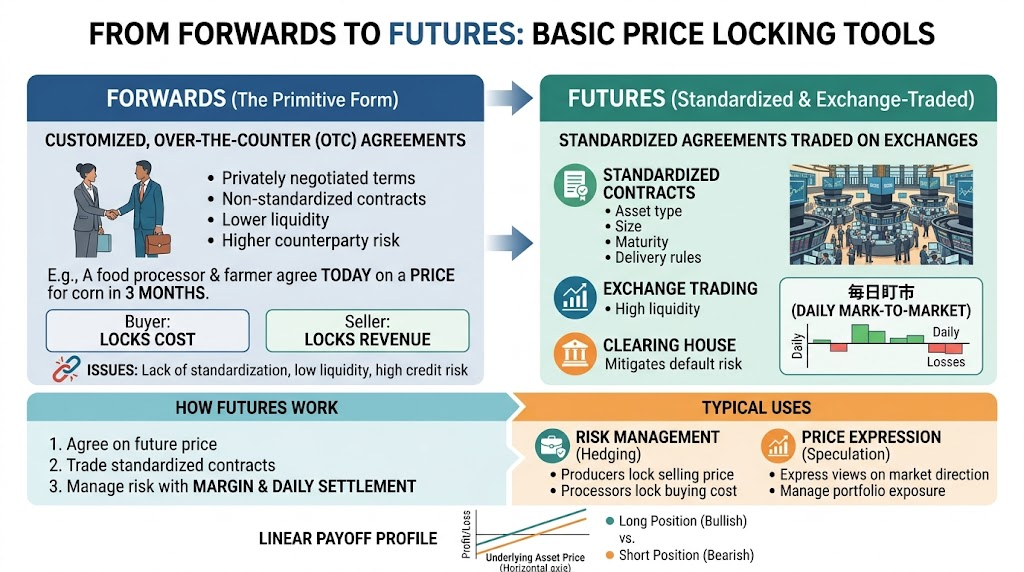

To understand futures, it’s best to start with “forwards.” A forward contract can be seen as one of the earliest forms of derivatives. Its logic is simple: two parties agree today to buy or sell an asset at a certain price at a specific time in the future.

For example, a food processing company is concerned about raw material prices rising in three months, so today it agrees with its supplier on the purchase price three months from now. This way, regardless of how the market price fluctuates, both parties can complete the transaction under the agreed conditions. For the buyer, costs are locked in; for the seller, revenue is secured.

The core function of a forward contract is to clarify the terms of a future transaction, but it also has obvious issues:

- Contracts are typically privately negotiated and lack standardization

- Liquidity is low, making them hard to transfer at will

- If one party defaults, the other bears significant credit risk

Due to these limitations, the market gradually developed more standardized futures contracts.

What are futures?

Futures can be understood as “standardized, exchange-traded forward contracts.” They also specify trading an asset at a certain price in the future, but unlike forwards, futures are usually listed on exchanges with highly standardized contract terms, such as:

- What is the underlying asset

- Contract size

- When does it expire

- How delivery is arranged

The main benefit of standardization is that it greatly expands market size and increases liquidity. Participants don’t need to negotiate each contract; they can directly buy and sell contracts of uniform specifications.

How do futures work?

The basic operation of futures can be summarized in three points:

- Both parties agree on a future price for a transaction

- Contracts are standardized and traded on exchanges

- Risk is managed through margin and daily mark-to-market mechanisms

“Mark-to-market” is very important here. Unlike the common misconception of “settling only at expiration,” futures markets typically settle account profits and losses daily based on price fluctuations. This means gains and losses from price changes are constantly reflected in accounts, reducing default risk.

Typical uses of futures

Futures are the most basic derivative tool because they are suitable for both risk management and price expression.

Common uses include:

- Producers lock in future selling prices

- Buyers lock in future purchase costs

- Investors express views on future price directions

- Institutions manage market exposure within asset portfolios

Essentially, futures address the problem of “uncertain future prices.” Their return structure is generally linear: when the underlying price rises, long positions benefit; when prices fall, short positions benefit.

Perpetual Contracts: Futures Without an Expiration Date

Based on traditional futures contracts, perpetual contracts are a special type of futures widely used in the cryptocurrency market. Unlike traditional futures, perpetual contracts have no fixed expiration date, allowing investors to hold positions long-term without worrying about contract expiry.

Features of perpetual contracts

- No expiration date: Perpetual contracts have no set delivery date; investors can enter or exit the market at any time based on market conditions. With no expiry restriction, they are closer to spot trading.

- Funding fee: To keep perpetual contract prices close to spot prices, trading platforms periodically (usually every 8 hours) adjust contract prices through funding fees paid or received to balance price deviations between longs and shorts. Funding fees are typically calculated based on differences between contract market prices and spot prices.

- If the contract price is higher than the spot price, shorts pay funding fees to longs; if lower, longs pay fees to shorts.

- Margin and leverage: Perpetual contracts allow leverage; investors can amplify their trading exposure by providing margin. Leverage lets investors take on larger market risks with relatively small capital.

- Suitable for rapid trading: Without an expiration date, perpetual contracts are especially suitable for short-term speculators and arbitrageurs. Investors can enter and exit the market at any time without worrying about settlement risks from contract expiry.

Differences between perpetual contracts and traditional futures

- Expiration date: Traditional futures have a set expiration date; perpetual contracts do not.

- Settlement method: Traditional futures settle via physical delivery or cash settlement at expiration; perpetual contracts use funding fees to maintain consistency with spot prices.

- Trading flexibility: Perpetual contracts offer greater flexibility and can be bought or sold at any time, ideal for frequent trading.

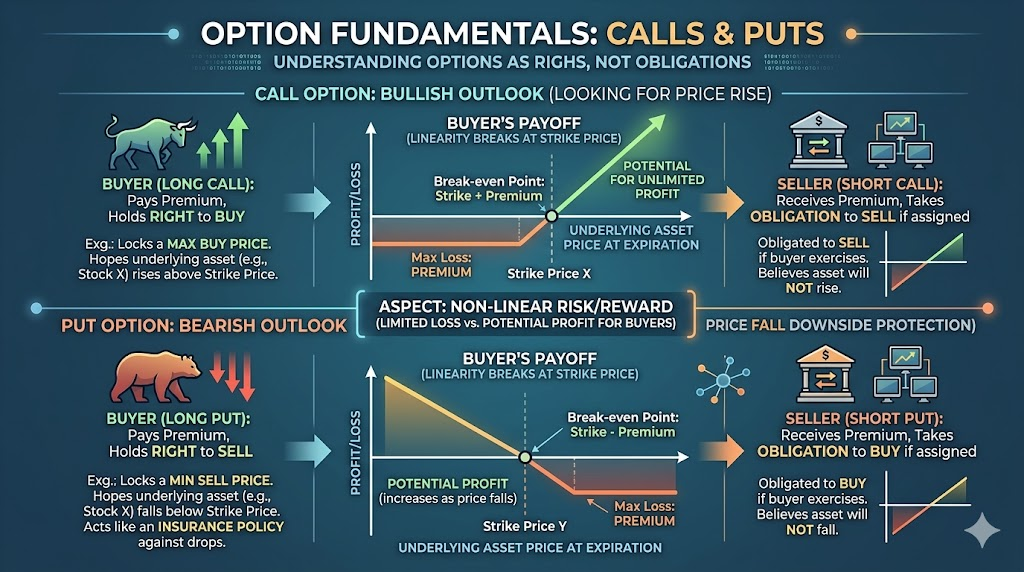

II. Options: Asymmetric Tools Designed Around “Rights”

If futures are contracts where both parties assume obligations, the core of options is “separating rights from obligations.”

What are options?

An option gives the buyer the right—but not the obligation—to buy or sell an asset at an agreed price at or within a certain future time. The seller must fulfill the contract if the buyer exercises this right.

The key phrase here is “right but not obligation.” This means that option buyers can decide whether or not to exercise their right depending on future market conditions. If market moves favor them, they can exercise; if not, they can abandon the option—their maximum loss is usually limited to the premium paid upfront.

Two basic types of options

The two most basic types of options are:

- Call option: Gives the buyer the right to buy an asset at an agreed price in the future

- Put option: Gives the buyer the right to sell an asset at an agreed price in the future

This structure makes options ideal for constructing asymmetric risk-return profiles. For example, if an investor fears their stock will drop but doesn’t want to sell it, they can buy a put option to hedge downside risk. If prices fall, option gains can offset some spot losses; if prices rise, upside potential is retained.

Why are options important?

Options matter because they provide a more flexible way to manage risk than futures. Futures are better for locking in prices directly; options are better for managing “tail risk” or structuring “limited loss with retained upside.”

A simple comparison:

- Futures are like direct commitments for future transactions

- Options are like buying insurance against future uncertainty

- Futures returns are more linear

- Options returns are more asymmetric

Thus, options play a crucial role in institutional risk management, volatility trading, and complex strategy design.

Practical significance of options

Options are vital in modern finance not because they’re complex but because they allow participants to manage risk more precisely. They let investors answer questions such as:

- I’m worried about a big price drop but don’t want to give up gains—what should I do?

- I think the market will be volatile but am unsure about direction—what should I do?

- I want to earn income but am willing to take on some conditional performance risk—what should I do?

Spot and simple futures often can’t elegantly solve these problems; options provide a more refined toolbox.

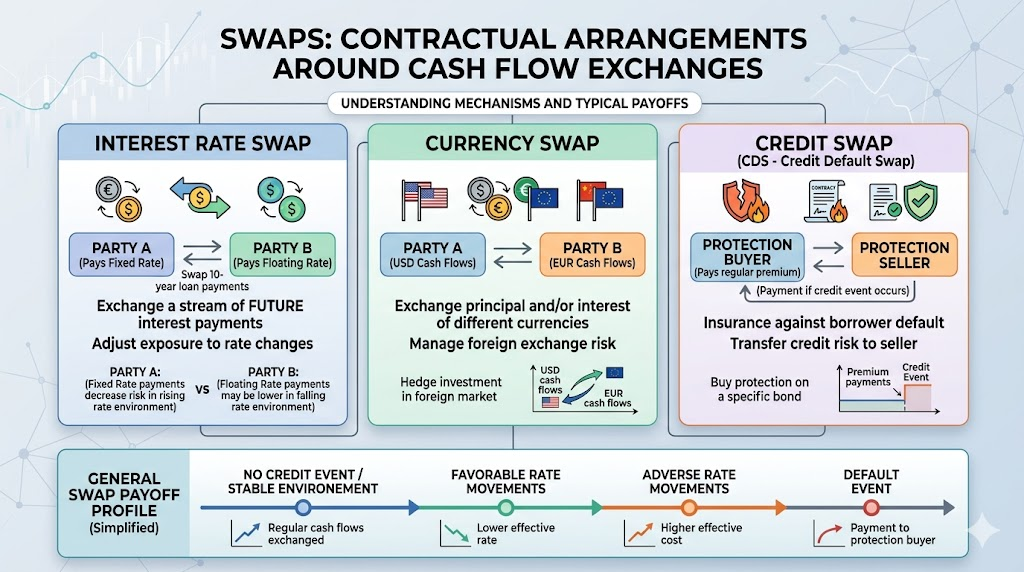

III. Swaps: Contracts Arranged Around Cash Flow Exchanges

Compared with futures and options, swaps are less visible among retail investors but serve as critical tools in institutional finance.

What is a swap?

A swap essentially involves two parties exchanging certain cash flow arrangements over a period in the future. It’s usually not about a one-time delivery but about ongoing payment structures.

The most common swaps include:

- Interest rate swaps

- Currency swaps

- Credit swaps

For example, in an interest rate swap, one party might pay a fixed rate while the other pays a floating rate. By exchanging cash flows, both parties adjust their exposure to interest rate changes.

Why do swaps exist?

The reason is simple: Many financial risks aren’t one-off price changes but ongoing cash flow risks.

For example:

- A company financing itself may worry about rising floating rates

- A multinational may worry about exchange rate volatility affecting long-term payments

- Financial institutions may need to realign asset-liability risk structures

These scenarios involve changes over time rather than just “one-day price moves.” Therefore, swaps are better suited for medium-to-long-term structured risk management needs than futures or options.

Market characteristics of swaps

Unlike highly standardized exchange-traded futures, many swaps have historically been traded over-the-counter (OTC), with more flexible terms tailored to institutional needs. This also means:

- Counterparty credit risk deserves more attention

- Contract structures may be more complex

- Market transparency is typically lower than for exchange-traded products

However, their flexibility makes swaps indispensable tools in institutional finance.

IV. What’s Different About These Three Tools?

To understand futures, options, and swaps, what matters most isn’t memorizing definitions but grasping how their risk organization methods differ.

Compare them from three perspectives:

- Structure of rights and obligations

- Futures: Both buyer and seller bear contractual obligations

- Options: Buyer holds rights; seller assumes obligations

- Swaps: Both parties exchange future cash flows as agreed

- Risk-return structure

- Futures: Typically linear profit and loss relationship

- Options: Usually asymmetric profit and loss relationship

- Swaps: Focused on ongoing adjustment of risk exposure and cash flow structure

- Applicable scenarios

- Futures: Best for locking in prices or expressing directional views

- Options: Best for managing tail risks and retaining flexibility

- Swaps: Best for managing long-term interest rate, currency, or credit risk

This explains why markets don’t just keep one type of derivative tool—because real-world risks aren’t all alike and participant needs go far beyond simply being “bullish or bearish.”

V. Why Do Different Markets Prefer Different Tools?

While all three tools are derivatives, different markets rely on them to varying degrees.

In commodities markets, futures are central since production, transport, and sales are directly impacted by future prices.

In equities and index markets, options tend to be more important since investors care about both direction and volatility/downside protection.

In institutional financing and cross-border finance, swaps are more critical because these contexts focus more on long-term cash flows and restructuring risk exposure.

In crypto markets, preferences show new features due to high volatility, frequent trading, and user structures oriented toward trading:

- Futures and perpetual contracts grow fastest

- The options market is growing but has higher barriers to entry

- Swap-like products often appear in other forms

This shows that derivatives’ popularity depends not just on product design but also on market structure, participant types, and risk management needs.

VI. From Tool Differences to Market Logic

Elevating this lesson’s content one step further reveals a key conclusion: The derivatives market isn’t “the more complex the tool, the more advanced,” but rather “the more diverse the risks, the more differentiated tools are needed.”

Risks in financial markets include at least:

- Price risk

- Volatility risk

- Interest rate risk

- Currency risk

- Credit risk

- Liquidity risk

Different tools emerge fundamentally to slice up and address these risks more precisely. Futures suit directional price risk; options handle asymmetric risks and extreme volatility; swaps manage long-term cash flow exposure. The richer the toolbox, the better markets can reallocate risks to those most willing—and able—to bear them.

This is the underlying logic driving ongoing expansion in derivatives markets.

VII. Lesson Summary

This lesson introduced three core derivative instruments: futures, options, and swaps. While all serve risk management and future planning purposes, their structures differ significantly. Futures focus on standardized forward price-locking; options emphasize asymmetric returns after separating rights from obligations; swaps focus on ongoing cash flow exchanges and risk restructuring.

With an understanding of these three tools, we see that derivatives markets aren’t single-product markets—they’re systems built around diverse risk needs. The need for multiple derivatives isn’t because finance loves complexity but because real-world risks come in different forms.

In the next lesson, we’ll discuss another key question: Who uses derivatives? We’ll break down market participant structures—from hedgers to speculators to arbitrageurs and market makers—and explore how prices form through multi-party competition.