Having understood the definition of derivatives, tool structures, participant dynamics, and core functions, we can now answer a more practical question: Why do “risk management and price discovery” give rise to different product forms in traditional finance versus crypto markets?

Many people view crypto contracts as “high-volatility, high-leverage” trading tools. But at a deeper level, crypto derivatives are not disconnected “new species”—they are the same risk organization logic re-engineered for a new market structure. In other words, core functions like risk transfer, price discovery, and liquidity organization remain unchanged; what differs is the operating environment: trading hours, participant structure, collateral systems, clearing mechanisms, and platform infrastructure.

I. Understand One Core Fact First: Crypto Markets Replicate Not “Product Form” but “Functional Core”

In traditional markets, futures, options, and swaps exist because each serves different risk needs. These needs persist—and even intensify—in crypto due to higher volatility, more continuous trading, and faster asset flows.

For example: miners need to lock in future income; long-term holders need to manage drawdown risk; market makers need to hedge inventory exposure; institutions need to manage portfolio volatility. As long as these needs exist, derivatives will emerge.

Therefore, crypto derivatives are not mechanically copied from traditional tools—they represent a reengineering of traditional functions within a “24/7 global matching and clearing platform-centric system.”

II. The Three Main Types of Crypto Derivatives: Delivery Futures, Perpetual Swaps, and Options

Currently, the most common crypto derivatives fall into three categories:

- Delivery Futures: Similar logic to traditional futures—have an expiry date—suitable for expressing price views at a specific point in time or for hedging.

- Perpetual Swaps: The most representative innovation in crypto markets. No expiry date; funding rate mechanisms keep contract prices anchored around spot.

- Options: Provide asymmetric risk management—used for downside protection, volatility plays, or yield-enhancement strategies.

These three product types serve three core needs:

- Delivery futures focus on “locking in prices at specific times”;

- Perpetual swaps focus on “expressing directional views with high liquidity and continuous trading”;

- Options focus on “fine-tuned risk management and structured strategy design.”

III. Why Did Perpetual Swaps Quickly Become Mainstream in Crypto Markets?

If traditional markets center on “term structure management,” then one major feature of crypto is “continuous trading demand.” Perpetual swaps fit this perfectly.

Their key mechanism is the funding rate: when contract prices exceed spot prices, longs typically pay shorts; vice versa when shorts pay longs. This does not directly determine direction but gradually converges contract prices toward spot over time.

Perpetual swaps’ popularity is no accident—they simultaneously offer:

- Trading convenience: no rollover costs at expiry—ideal for high-frequency or short/medium-term trading;

- Capital efficiency: margin systems boost capital utilization;

- Market depth: active trading enables quick entry/exit and effective hedging.

Their convenience also leads to overuse—a critical point for later risk management lessons: convenience does not mean low risk.

IV. Similarities and Differences Between Crypto Derivatives and Traditional Markets

Similarities:

- Both focus on risk transfer and price discovery;

- Both rely on hedging, speculation, arbitrage, and market making roles working together;

- Both require standardized clearing mechanisms to control default and systemic risks.

Differences:

- Trading hours differ: crypto runs 24/7 with risks emerging at any time;

- Collateral differs: traditional markets use fiat or low-volatility assets for margin; crypto uses higher-volatility collateral;

- Microstructure differs: platform rules (funding rates, liquidation mechanisms, risk limits) have more direct impact on short-term price behavior in crypto;

- Participant composition differs: retail dominates crypto; positions shift faster; sentiment transmission is more sensitive.

These differences mean that even products with the same name may have significantly different risk characteristics and trading behaviors.

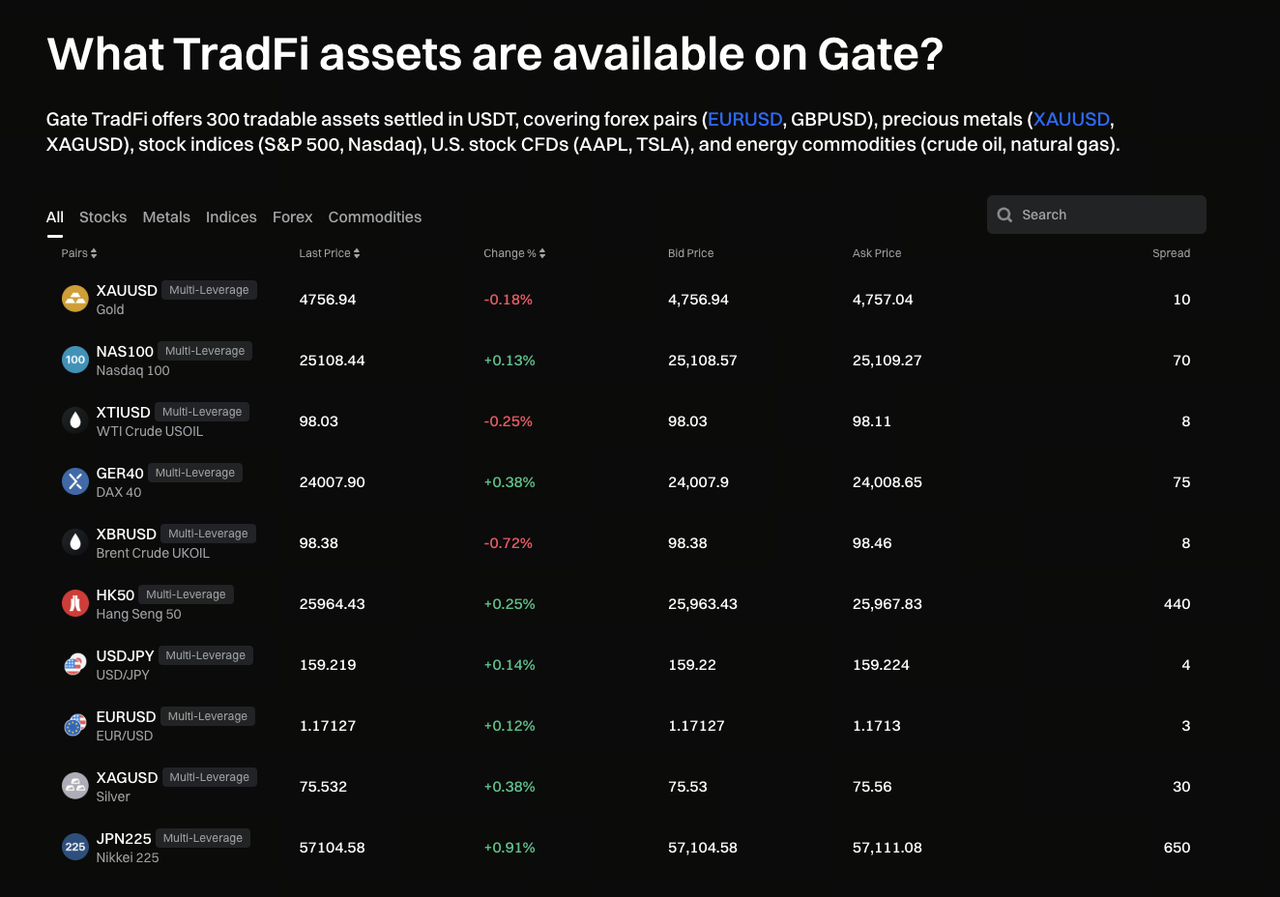

V. Gate TradFi: A Practical Entry Point Bridging Traditional Asset Logic with Crypto Trading Ecosystems

Image source: Gate TradFi page

As “traditional financial logic” and “crypto market structure” gradually merge, platform-level products begin serving as bridges.

Gate TradFi can be seen as such a bridging module—it introduces aspects of traditional asset trading and risk management logic into an environment more familiar to digital asset users. This allows users to access broader risk exposures and asset classes within one platform ecosystem.

For learners, Gate TradFi’s significance goes beyond “an extra tradable asset class.” More importantly, it helps users develop cross-market perspectives:

- Traditional asset prices do not operate in isolation—they fluctuate with interest rate expectations, macro liquidity, and risk appetite;

- Digital assets are not absolutely disconnected from traditional assets—correlations may strengthen at times with capital flows and risk resonance;

- For portfolio management, cross-market tools allow more refined arrangement of exposures—not concentrating all risks in one asset class.

Gate TradFi’s value lies in naturally introducing “the language of traditional financial risk pricing” into the crypto user context—helping users shift from single-trader thinking toward multi-asset, cross-cycle, cross-market portfolio thinking.

VI. How to Choose Tools in Practice: Identify “Risk Problem” First—Then Select “Product”

Many beginners reverse the process—first checking which product is hot before figuring out how to use it. The better sequence is:

- Ask yourself what type of risk you face (directional risk, volatility risk, tail risk, liquidity risk);

- Then decide which tool type to use (delivery futures, perpetual swaps, options);

- Finally determine leverage level, term length, and position sizing.

A practical rule:

- For simple directional expression and fast execution—perpetuals are usually more efficient;

- For precise risk management at a specific time—delivery futures are clearer;

- To control downside while retaining upside—options are most suitable.

No tool is inherently “superior”—only whether it matches your current risk objectives.

VII. Lesson Summary

The key conclusion of this lesson is: while crypto derivatives markets seem new—the problems they solve are not—they remain focused on risk transfer, price discovery, and liquidity organization. What has truly changed are the market environment and mechanism implementations.

We analyzed the three main tools—delivery futures, perpetual swaps, options—explained why perpetuals have become central in crypto markets, and outlined both functional similarities and structural differences between traditional and crypto derivatives.

We also introduced Gate TradFi as a bridge scenario—not just expanding product offerings but helping users build a cross-market risk cognition framework.

In the next lesson we’ll move toward course conclusions—discussing opportunities, key risks, future trends in crypto derivatives markets—and providing actionable learning paths for further advancement.