As AI technology migrates from cloud-based computing power to edge devices, a major shift is underway: smartphones are entering a new hardware upgrade cycle.

Unlike previous cycles, the impetus is no longer just raw performance gains — AI functions now demand superior camera systems, sensors, and image processing. Capabilities like AI-powered image recognition, real-time enhancement, and computational photography have elevated the camera from a mere "recording tool" to an "AI input portal."

Within this structural shift, LG Innotek has become one of the most direct beneficiaries among South Korean companies.

How the AI iPhone Upgrade Cycle Is Reshaping the Camera and Optics Supply Chain

The smartphone industry has seen a notable "replacement cycle elongation" over the past few years, but AI is reversing that trend. Apple is driving an upgrade of the AI iPhone ecosystem, encompassing not just software but also hardware-level system improvements — higher-resolution cameras, more complex multi-camera arrays, and stronger image processing engines.

In this context, the camera module regains critical importance: it's no longer just for capturing photos but serves as the data input source for AI.

As a result, the entire optics supply chain is pivoting from "hardware component delivery" to "AI perception gateway provider."

LG Innotek's Core Business Structure: From Camera Modules to Semiconductor Substrates

LG Innotek's business breaks down into three main segments:

- Camera Module Business: The company's primary revenue engine, supplying Apple iPhones for both front and rear camera systems. This segment has historically accounted for over 70% of total revenue.

- Optical and Sensing Solutions: Includes OIS (Optical Image Stabilization) systems, 3D sensing components, and next-generation optical technology development.

- Semiconductor Substrate Business (e.g., FC-BGA): Targets servers and high-performance computing, representing a medium-to-long-term growth avenue.

Notably, the company is reducing its reliance on a single customer by expanding into automotive electronics and server chip packaging, hedging against smartphone cycle volatility.

Recent Market Drivers: Apple Cycle + Margin Recovery + Foreign Inflows

In the South Korean market, LG Innotek's stock has shown a clear structural uptrend, driven by three core factors:

- Stronger Order Expectations from the Apple iPhone AI Upgrade Cycle: The market anticipates AI features will boost high-end iPhone sales, driving demand for premium camera modules.

- Profit Recovery Outlook: Analysts expect margin improvement in camera modules as the mix shifts toward high-end models, with overall profitability entering a recovery phase.

- Foreign Capital Inflows: Data shows that even during pullbacks, foreign investors have increased positions in core supply chain plays like LG Innotek, reflecting their rising allocation value in the AI smartphone narrative.

Structurally, this rally is not short-term speculation but a convergence of the "Apple cycle + AI feature upgrades + profit recovery."

Technology Upgrade Logic: How Multi-Camera Systems and Premiumization Boost Per-Device Value

LG Innotek's long-term value is tied to smartphone camera evolution.

Smartphones are moving from single or dual cameras to multi-camera fusion and computational photography. AI further amplifies the camera's role as a system-level sensing input. Meanwhile, a higher mix of premium models raises the camera value per device. Analysts believe that within Apple's lineup, a greater share of high-end iPhones directly enhances LG Innotek's revenue structure and margins.

Additionally, the company is advancing packaging and optics innovations like copper post packaging for improved module density and heat dissipation, further strengthening its competitive moat.

Position in the Korean Electronics Supply Chain: LG Innotek's Indispensability

In the Korean electronics ecosystem, LG Innotek is a classic "core high-end component supplier."

It doesn't sell directly to consumers, but its parts are essential to premium smartphones and computing devices. Within Apple's supply chain, its camera modules hold a dominant share.

At the same time, its optics and semiconductor packaging footprint positions it to transition from a "consumer electronics supplier" to an "AI device infrastructure provider."

This structural transformation gives it lasting relevance in the AI edge-computing trend.

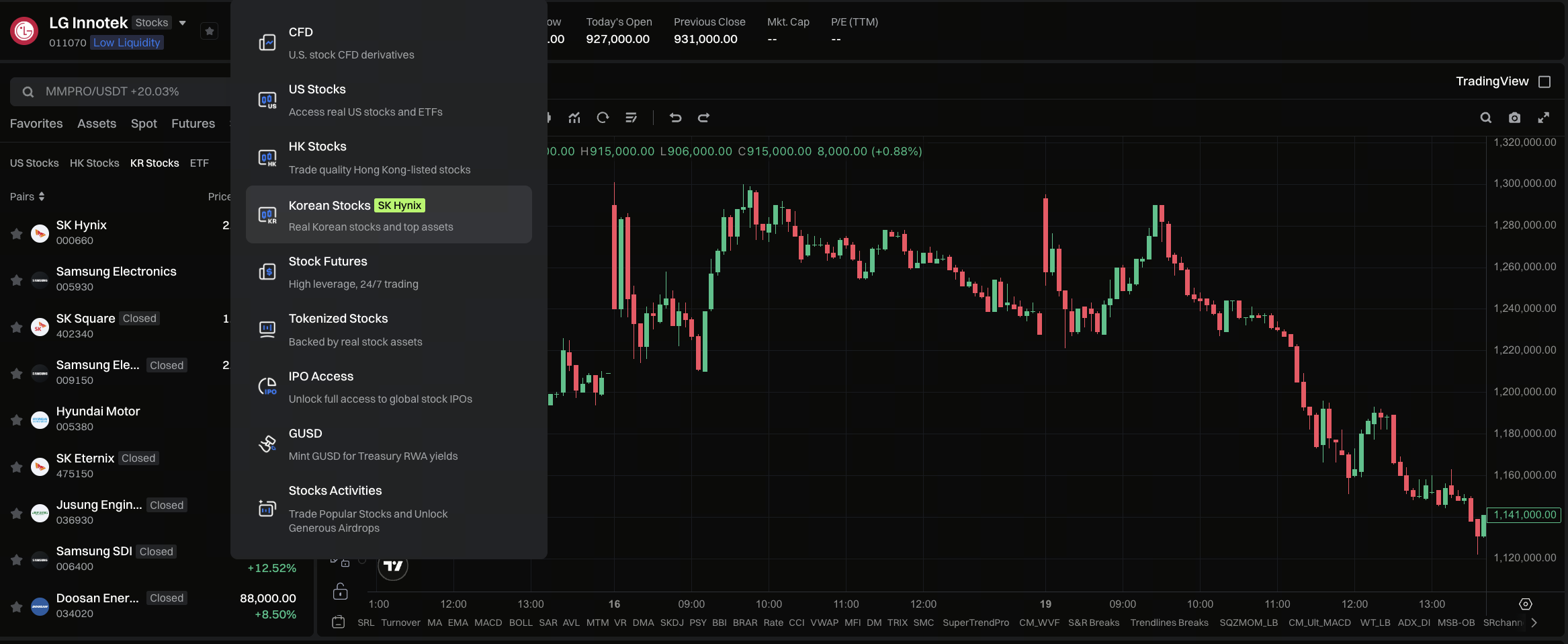

How Gate's Korean Stock Trading Connects to the LG Innotek Investment Opportunity

With Gate's launch of South Korean stock trading, investors can trade KOSPI stocks like LG Innotek through a unified account system.

Key changes this system brings:

- Unified pricing and settlement in USDT

- Integration of U.S., Hong Kong, and South Korean stocks

- Lower barriers for cross-border account opening

- Enhanced global asset allocation efficiency

For investors, this means Apple supply chain assets in South Korea are no longer a regional play — they can be part of a global portfolio.

Step-by-Step Guide to Investing in LG Innotek on Gate

In practice, the process simplifies to standard steps within a unified account system. Users first register and complete identity verification to obtain stock trading access. Then, they transfer USDT from their spot wallet to the stock account as trading capital.

After entering the KOSPI market, searching for "LG Innotek" or its ticker brings up the trading interface. Orders can be placed as market or limit orders. Once executed, positions are automatically managed in a consolidated asset view alongside other market holdings, enabling cross-market portfolio management.

Valuation Shift: From Cyclical Stock to AI Device Chain Core Asset

LG Innotek's valuation logic is evolving. Historically, the market treated it as a cyclical consumer electronics stock, tightly correlated with iPhone sales. But in the AI smartphone era, its role is shifting to an "AI terminal hardware supplier."

The implication: a higher valuation multiple. The market is beginning to price it as part of the AI device chain, not just a component maker.

Risk Profile: Customer Concentration and Apple Dependence

Despite its growth narrative, LG Innotek carries structural risks.

The primary risk is customer concentration: Apple accounts for the vast majority of its revenue. Any downturn in the iPhone sales cycle directly impacts its financials.

Moreover, the smartphone market is mature with limited long-term expansion, so its cyclical characteristics remain pronounced.

Conclusion: The Underappreciated Winner of the AI Smartphone Era

LG Innotek is at a structural inflection point.

As AI moves from the cloud to the edge, the importance of cameras and optics continues to rise, transforming the company from a traditional component supplier into a core AI input enterprise.

With Gate integrating South Korean stocks into its unified trading platform, global investors can now more directly participate in the revaluation of this AI terminal supply chain.

FAQs

-

Q1: What is LG Innotek's main business?

Camera modules, optical solutions, and semiconductor substrates.

-

Q2: Why is it affected by AI?

AI smartphones need advanced camera systems as input sensors.

-

Q3: Who is its biggest customer?

Primarily Apple for its iPhone line.

-

Q4: Do I need a Korean broker to trade on Gate?

No, you can trade Korean stocks directly on the platform.

-

Q5: Is it more of a growth or cyclical stock?

It's a hybrid — driven by both cyclical factors and AI upgrade momentum.