Trade

Basic

Futures

Futures

Hundreds of contracts settled in USDT or BTC

TradFi

Gold

Trade global traditional assets with USDT in one place

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Participate in events to win generous rewards

Demo Trading

Use virtual funds to experience risk-free trading

Earn

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and enjoy airdrop rewards!

Futures Points

Earn futures points and claim airdrop rewards

Investment

Simple Earn

Earn interests with idle tokens

Auto-Invest

Auto-invest on a regular basis

Dual Investment

Buy low and sell high to take profits from price fluctuations

Soft Staking

Earn rewards with flexible staking

Crypto Loan

0 Fees

Pledge one crypto to borrow another

Lending Center

One-stop lending hub

VIP Wealth Hub

Customized wealth management empowers your assets growth

Private Wealth Management

Customized asset management to grow your digital assets

Quant Fund

Top asset management team helps you profit without hassle

Staking

Stake cryptos to earn in PoS products

Smart Leverage

New

No forced liquidation before maturity, worry-free leveraged gains

GUSD Minting

Use USDT/USDC to mint GUSD for treasury-level yields

More

CEO

🇺🇸 President Trump says the U.S. economy will surge by 15% or more if Kevin Warsh cuts interest rates.

- Reward

- 2

- Comment

- Repost

- Share

Viewing the Top Market Coins Spot Chart and comparing them

469

- Reward

- 8

- 5

- Repost

- Share

ybaser :

:

Happy New Year! 🤑View More

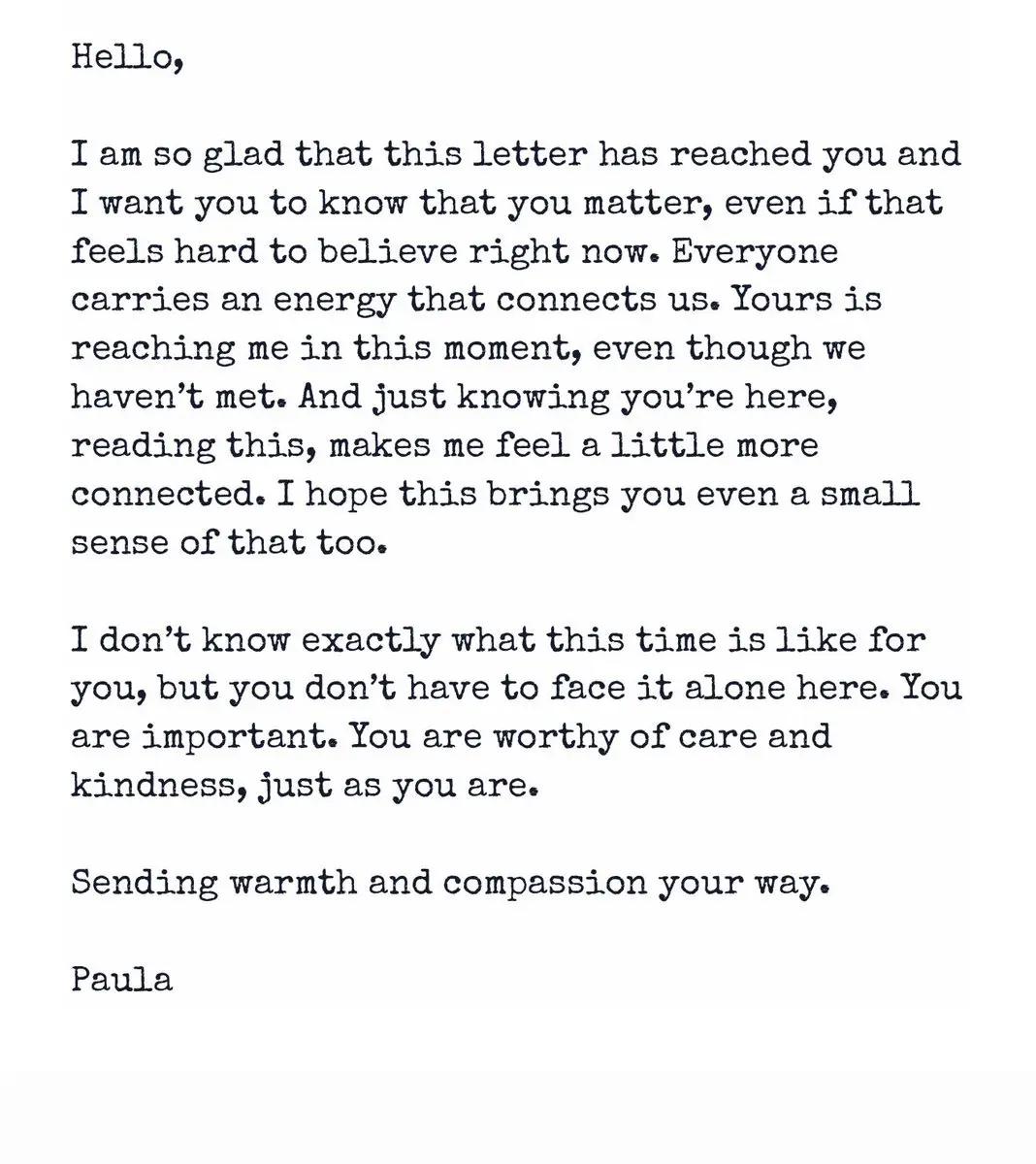

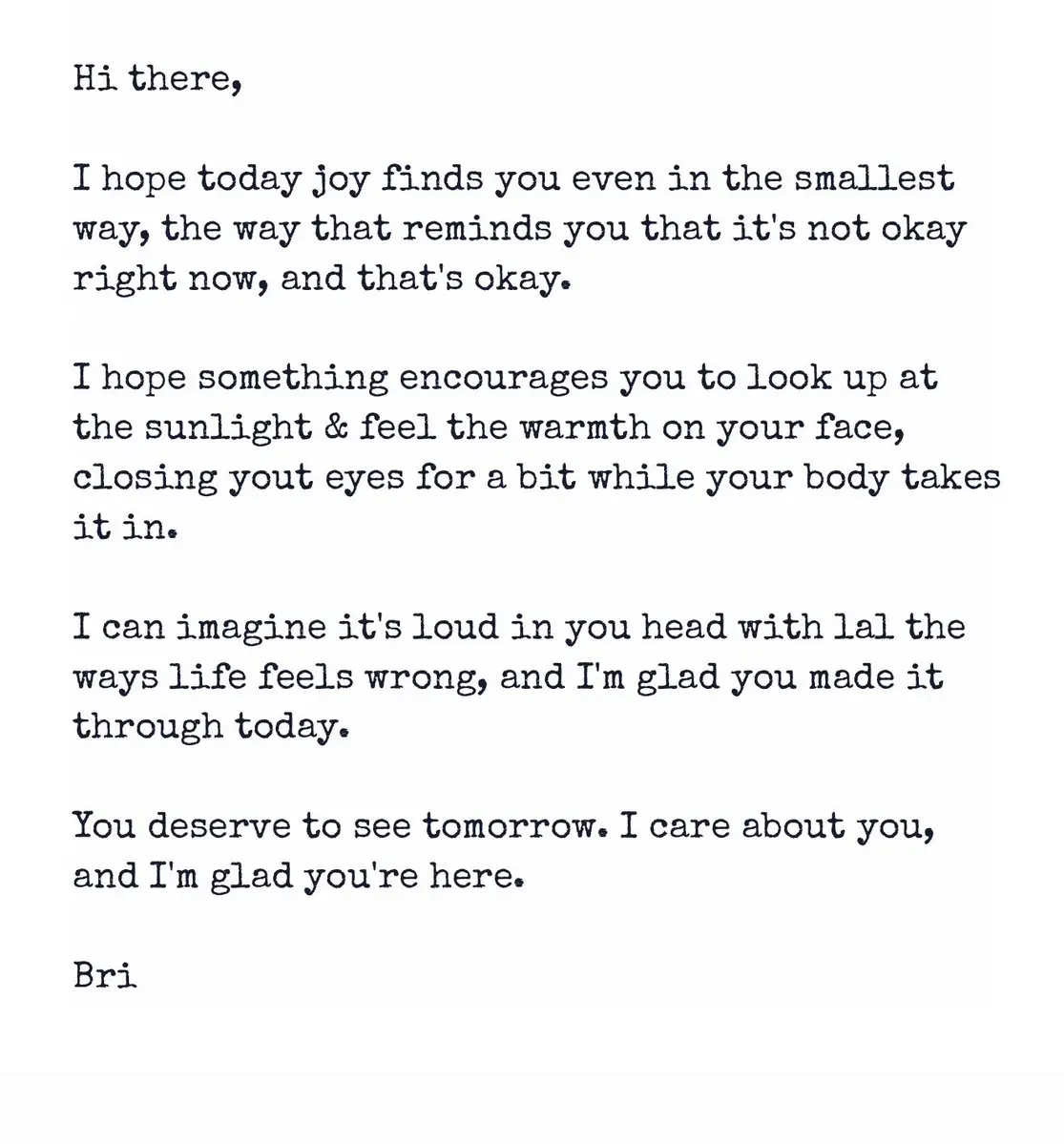

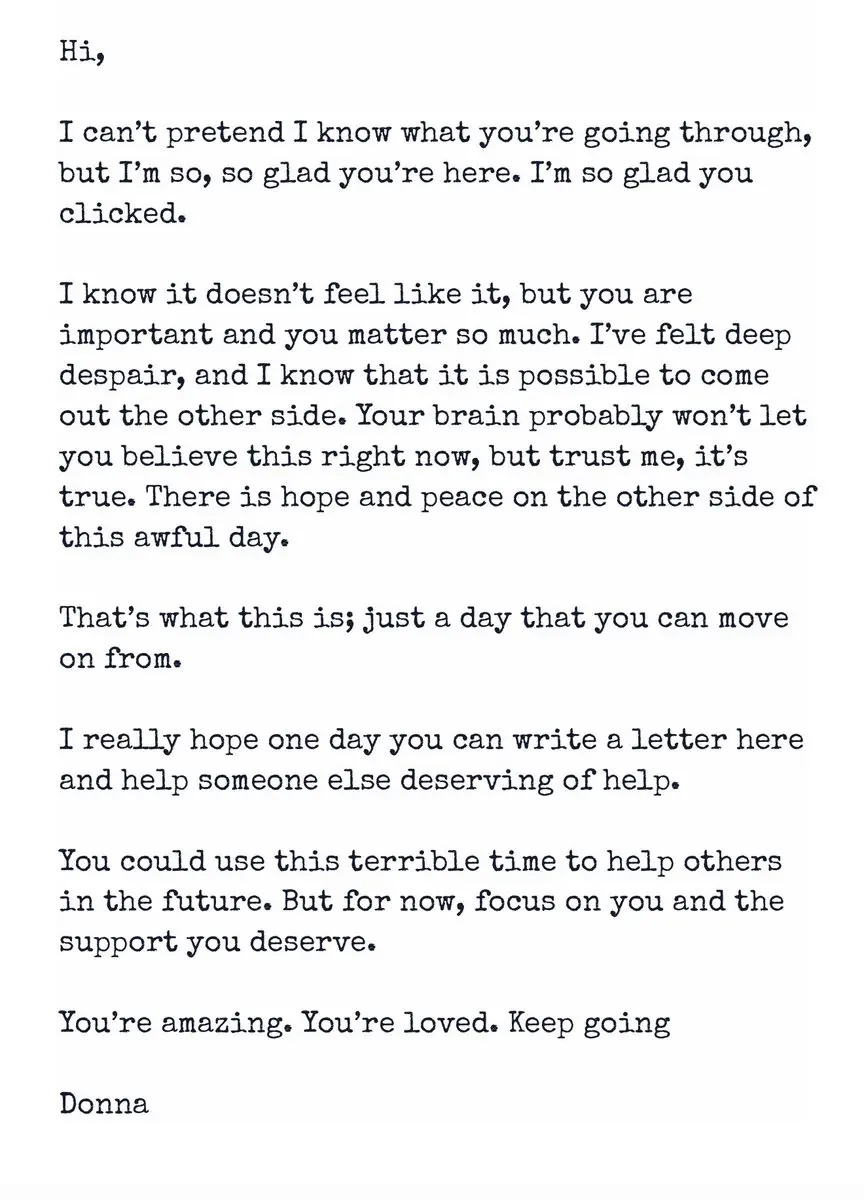

A guy went viral for creating a website called “reasons to stay” where anonymous people write letters to people who need a moment of hope. He did this in honour of his little brother who took his own life 8 years ago.

If you are struggling, I highly recommend checking it out.

If you are struggling, I highly recommend checking it out.

- Reward

- like

- Comment

- Repost

- Share

p小将

p小将

Created By@DreamJourney

Listing Progress

100.00%

MC:

$1.76K

More Tokens

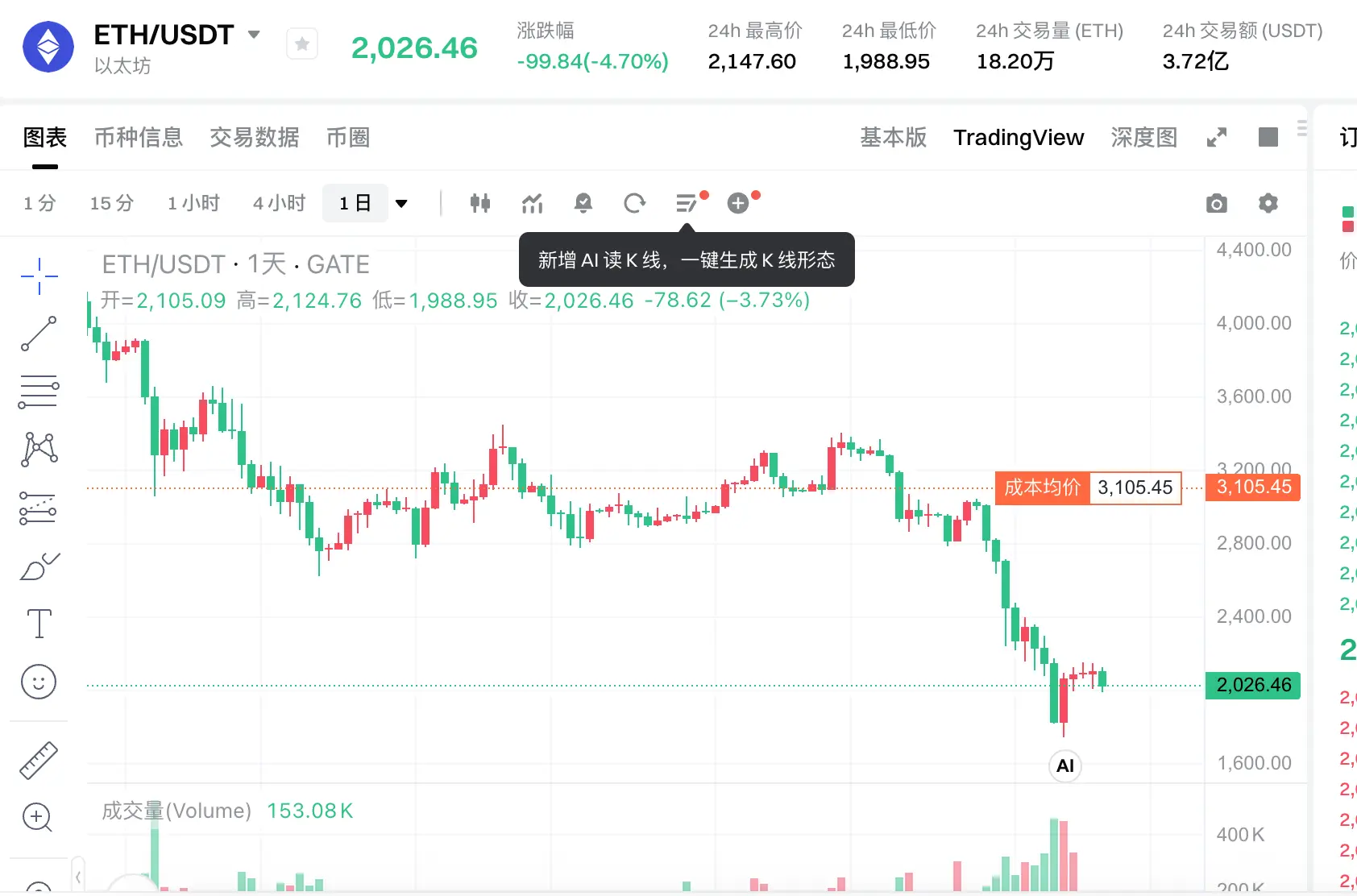

Currently, Bitcoin and ETH are: declining with increased volume, and rebounding with decreased volume!

This is a typical bearish market structure!

The main reason for this phenomenon is that a large amount of capital is actively selling, including long stop-losses/forced liquidations, big players selling, and trapped positions being unwound—all essentially capital fleeing the market.

The rebound with decreased volume is mainly short covering, small-scale bottom fishing, and technical repairs, but no large funds are entering.

It can be said that currently, declining with increased volume = genu

View OriginalThis is a typical bearish market structure!

The main reason for this phenomenon is that a large amount of capital is actively selling, including long stop-losses/forced liquidations, big players selling, and trapped positions being unwound—all essentially capital fleeing the market.

The rebound with decreased volume is mainly short covering, small-scale bottom fishing, and technical repairs, but no large funds are entering.

It can be said that currently, declining with increased volume = genu

- Reward

- like

- Comment

- Repost

- Share

- Reward

- 1

- Comment

- Repost

- Share

- Reward

- like

- 1

- Repost

- Share

Changmin:

In the future, avoid these kinds of sharp fluctuations. Avoid them.

- Reward

- like

- Comment

- Repost

- Share

Participate in horse racing betting, complete tasks to earn horse racing tickets, and enjoy a million red envelope rain daily, sharing a prize pool of 100,000 USDT at the Gate 2026 Spring Festival Celebration. https://www.gate.com/competition/year-of-horse-2026?ref_type=165&utm_cmp=7EQB9Jba&ref=VGCVBG9AUW

View Original

- Reward

- 1

- Comment

- Repost

- Share

Participate in horse racing betting, complete tasks to earn horse racing tickets, and enjoy a million red envelope rain daily, sharing a prize pool of 100,000 USDT at the Gate 2026 Spring Festival Celebration. https://www.gate.com/competition/year-of-horse-2026?ref_type=165&utm_cmp=7EQB9Jba&ref=BVBNAw8

View Original

- Reward

- like

- Comment

- Repost

- Share

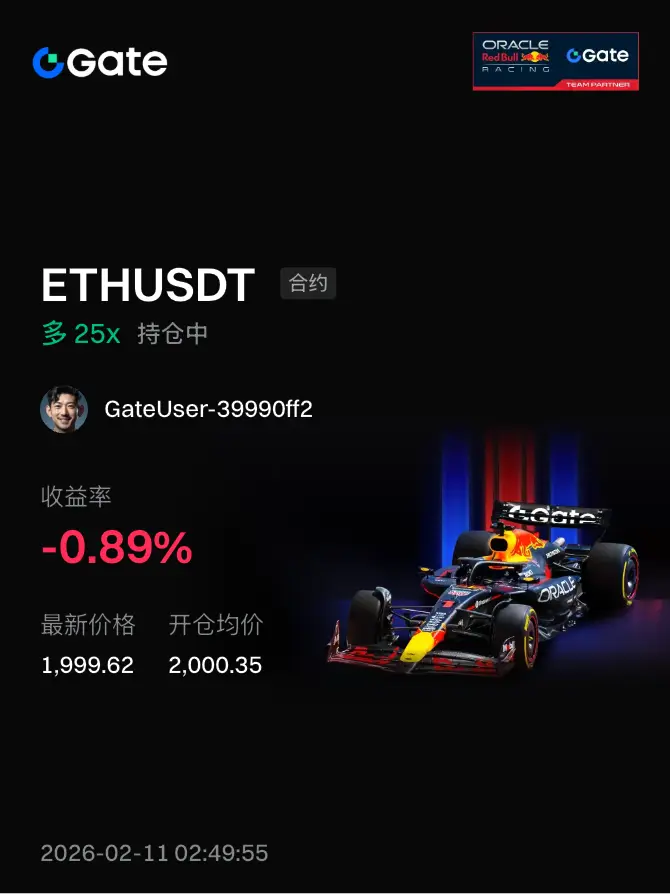

#Show my holdings' profit#当前行情抄底还是观望?

In this market, don't be ambitious. Just take a few points steadily and then run away.

View OriginalIn this market, don't be ambitious. Just take a few points steadily and then run away.

- Reward

- like

- Comment

- Repost

- Share

XAMD

XAMD

Created By@ViP2

Subscription Progress

0.00%

MC:

$0

More Tokens

Honest question:

Would it make more sense to incentivize with farms $MET liquidity primarily through a stable pair (MET/USDC) rather than MET/SOL?

My concern lately has been SOL downside risk spilling over into Meteora LPs. Even if MET fundamentals stay unchanged, SOL volatility directly impacts LP performance and impermanent loss.

From a market-structure perspective, anchoring the main liquidity pool to USDC could:

• Reduce exposure to SOL-driven volatility

• Make MET pricing more predictable

• Improve capital efficiency for LPs who want MET exposure without directional SOL risk

Notably, the

Would it make more sense to incentivize with farms $MET liquidity primarily through a stable pair (MET/USDC) rather than MET/SOL?

My concern lately has been SOL downside risk spilling over into Meteora LPs. Even if MET fundamentals stay unchanged, SOL volatility directly impacts LP performance and impermanent loss.

From a market-structure perspective, anchoring the main liquidity pool to USDC could:

• Reduce exposure to SOL-driven volatility

• Make MET pricing more predictable

• Improve capital efficiency for LPs who want MET exposure without directional SOL risk

Notably, the

- Reward

- like

- Comment

- Repost

- Share

Participate in horse racing betting, complete tasks to earn horse racing tickets, and enjoy a million red envelope rain daily, sharing a prize pool of 100,000 USDT at the Gate 2026 Spring Festival Celebration. https://www.gate.com/competition/year-of-horse-2026?ref_type=165&utm_cmp=7EQB9Jba&ref=VQRDUQHZUG

View Original

- Reward

- like

- Comment

- Repost

- Share

🚨 BITCOIN UPDATE:

THERE IS NO BID.

WE COULDN'T HOLD PREVIOUS ATH.

FIRST STOP: $65K

SECOND STOP: $62.5K

IF THERE'S STILL NO BID... WE'LL SEE SUB $60K VERY QUICKLY.

THERE IS NO BID.

WE COULDN'T HOLD PREVIOUS ATH.

FIRST STOP: $65K

SECOND STOP: $62.5K

IF THERE'S STILL NO BID... WE'LL SEE SUB $60K VERY QUICKLY.

BTC-2,4%

- Reward

- 1

- Comment

- Repost

- Share

Participate in horse racing betting, complete tasks to earn horse racing tickets, and enjoy a million red envelope rain daily, sharing a prize pool of 100,000 USDT at the Gate 2026 Spring Festival Celebration. https://www.gate.com/competition/year-of-horse-2026?ref_type=165&utm_cmp=7EQB9Jba&ref=VLJHVW0OCA

View Original

- Reward

- like

- Comment

- Repost

- Share

- Reward

- like

- Comment

- Repost

- Share

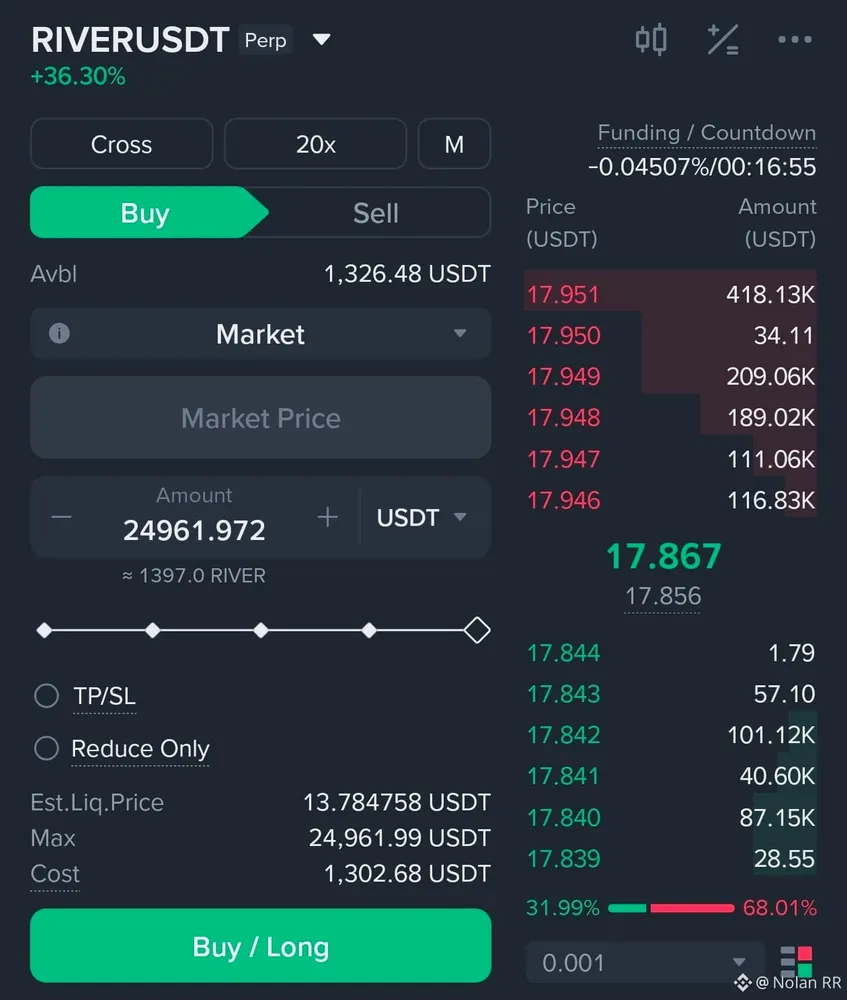

【$I'm coming, signal】Hold cash and observe - Bull trap under volume-price divergence

$I'm coming, after a surge with high volume, the price is consolidating at a high level, but there is dangerous resonance in the data.

🎯Direction: Hold cash

Market analysis: A single massive bullish candle on the 4H chart surged 16%, but the latest candlestick shows a long upper shadow, indicating heavy selling pressure around 0.0245. The key issue is: although the price has risen, the open interest trend (OI) remains "Stable" without synchronized increase, and the funding rate is as high as 0.0392%, indicati

View Original$I'm coming, after a surge with high volume, the price is consolidating at a high level, but there is dangerous resonance in the data.

🎯Direction: Hold cash

Market analysis: A single massive bullish candle on the 4H chart surged 16%, but the latest candlestick shows a long upper shadow, indicating heavy selling pressure around 0.0245. The key issue is: although the price has risen, the open interest trend (OI) remains "Stable" without synchronized increase, and the funding rate is as high as 0.0392%, indicati

- Reward

- like

- Comment

- Repost

- Share

Are you seeing what I’m seeing? All I see is green.

- Reward

- like

- Comment

- Repost

- Share

Load More

Join 40M users in our growing community

⚡️ Join 40M users in the crypto craze discussion

💬 Engage with your favorite top creators

👍 See what interests you

Trending Topics

View More210.98K Popularity

7.39K Popularity

10.15K Popularity

10.78K Popularity

5.08K Popularity

Hot Gate Fun

View More- MC:$0.1Holders:10.00%

- MC:$0.1Holders:10.00%

- MC:$0.1Holders:10.48%

- MC:$2.41KHolders:10.00%

- MC:$0.1Holders:10.00%

News

View MoreData: In the past 24 hours, the entire network has liquidated $227 million, with long positions liquidated at $156 million and short positions at $71.47 million.

7 m

Data: 2012.8 BTC transferred from an anonymous address, routed through a middle address, and then sent to another anonymous address

37 m

Data: If BTC breaks through $72,308, the total liquidation strength of mainstream CEX short positions will reach $1.117 billion.

1 h

Data: If ETH breaks through $2,103, the total liquidation strength of short positions on mainstream CEXs will reach $679 million.

1 h

Bitcoin Hashrate Drops 20% as Mining Profitability Collapses

1 h

Pin