Bitcoin Miners Pivot to AI Infrastructure as Hash Price Declines to $29/PH/s in Q1 2026

Bitcoin miners faced sustained margin compression in the first quarter of 2026, with hash price declining to approximately $29/PH/s per day, down from $36–38/PH/s in Q4 2025, as the network hashrate recovered to 1,020 EH/s following a 10% decline from its October 2025 peak of 1,160 EH/s.

Publicly listed miners have announced over $70 billion in cumulative AI and high-performance computing contracts, with several operators pivoting toward data center infrastructure that could account for up to 70% of their revenues by the end of 2026, fundamentally transforming the sector’s capital structure and risk profile.

AI Infrastructure Contracts Exceed $70 Billion as Miners Redeploy Power Capacity

The migration of Bitcoin miners toward AI and high-performance computing accelerated in Q4 2025 and early 2026, with publicly traded companies signing GPU co-location and cloud service deals with hyperscalers worth over $70 billion in aggregate. CoreWeave expanded its contract with Core Scientific to $10.2 billion over 12 years, with 350MW energized for HPC and full 590MW targeted by early 2027. TeraWulf reported $12.8 billion in total contracted HPC revenue across 522MW at its Lake Mariner facility.

Hut 8 signed a $7 billion, 15-year lease with Fluidstack for 245MW at its River Bend campus in Louisiana. Iris Energy scaled to over 10,900 NVIDIA GPUs, with AI Cloud Services revenue reaching $17.3 million in Q4 2025. Cipher Digital secured a multi-billion-dollar agreement with Fluidstack for its 300MW Barber Lake site, though revenue has not yet commenced.

The economic rationale for the shift is rooted in margin differentials. Hash price fell to $29/PH/s in early March 2026, compressing mining margins, while AI infrastructure offers structurally higher and more stable returns. Redeploying power and capital toward HPC appears rational for operators with access to scalable energy and existing data center capabilities. However, the transition is not uniform. CleanSpark continues to prioritize mining in the near term while gradually building AI exposure, and Marathon has deployed smaller containerized sites at the edge of energy networks suited for mining but incompatible with AI’s continuous uptime requirements.

Network Hashrate Declines 10% from October Peak before Recovering to 1,020 EH/s

The Bitcoin network surpassed 1 zetahash per second (ZH/s) in August 2025, peaking at approximately 1,160 EH/s in early October before declining 10% to 1,045 EH/s by late December 2025. The decline marked three consecutive negative difficulty adjustments, the first such streak since July 2022, driven by a 31% BTC price correction from its all-time high, rising winter energy costs, and renewed Chinese regulatory actions in Xinjiang during December 2025.

Hashrate recovered to approximately 1,020 EH/s by March 2026. The United States gained approximately 2 percentage points of market share quarter-over-quarter and now controls roughly 37.5% of global hashrate. The top three countries—the United States, China, and Russia—control approximately 68% of global hashrate. Emerging mining geographies including Paraguay, Ethiopia, and Oman entered the global top 10, driven by projects such as HIVE’s 300MW facility in Paraguay and Bitdeer’s 40MW operation in Ethiopia.

Using piecewise prediction models, analysts now expect the hashrate to achieve 1.8 ZH/s by the end of 2026 and 2 ZH/s by March 2027, one month later than previously predicted.

Hash Price Falls to $29/PH/s as Mining Economics Pressure Mid-Generation Hardware

Hash price, which measures miner revenue per unit of hashpower, declined steadily through Q4 2025 after peaking at $63/PH/s per day in July. By November, it had fallen to $35–37/PH/s, setting what was then a five-year low. A brief recovery to $38–40 in late December proved short-lived, with hash price collapsing to $28–30/PH/s by early March 2026, reaching new post-halving lows.

The decline resulted from record difficulty peaking at 155.97T in October 2025, depressed BTC price approximately 31% below its all-time high, and minimal transaction fee income consistently below 1% of total block rewards with average fees per block of approximately 0.018 BTC. At current hash price levels of $30/PH/s, miners running S19j Pro-class hardware at average industrial electricity costs of $0.05/kWh operate below breakeven. Approximately 15–20% of the global mining fleet is estimated to be unprofitable at current prices.

Publicly listed miners have collectively reduced their BTC treasuries by over 15,000 BTC from peak levels. Core Scientific sold approximately 1,900 BTC in January 2026 and plans to liquidate substantially all remaining holdings in Q1 2026. Bitdeer reduced its treasury to zero in February 2026, and Riot sold 1,818 BTC in December 2025. Marathon Holdings, which maintained a full HODL strategy in Q4, expanded its policy in March 2026 to authorize sales from its entire balance sheet reserve of 53,822 BTC.

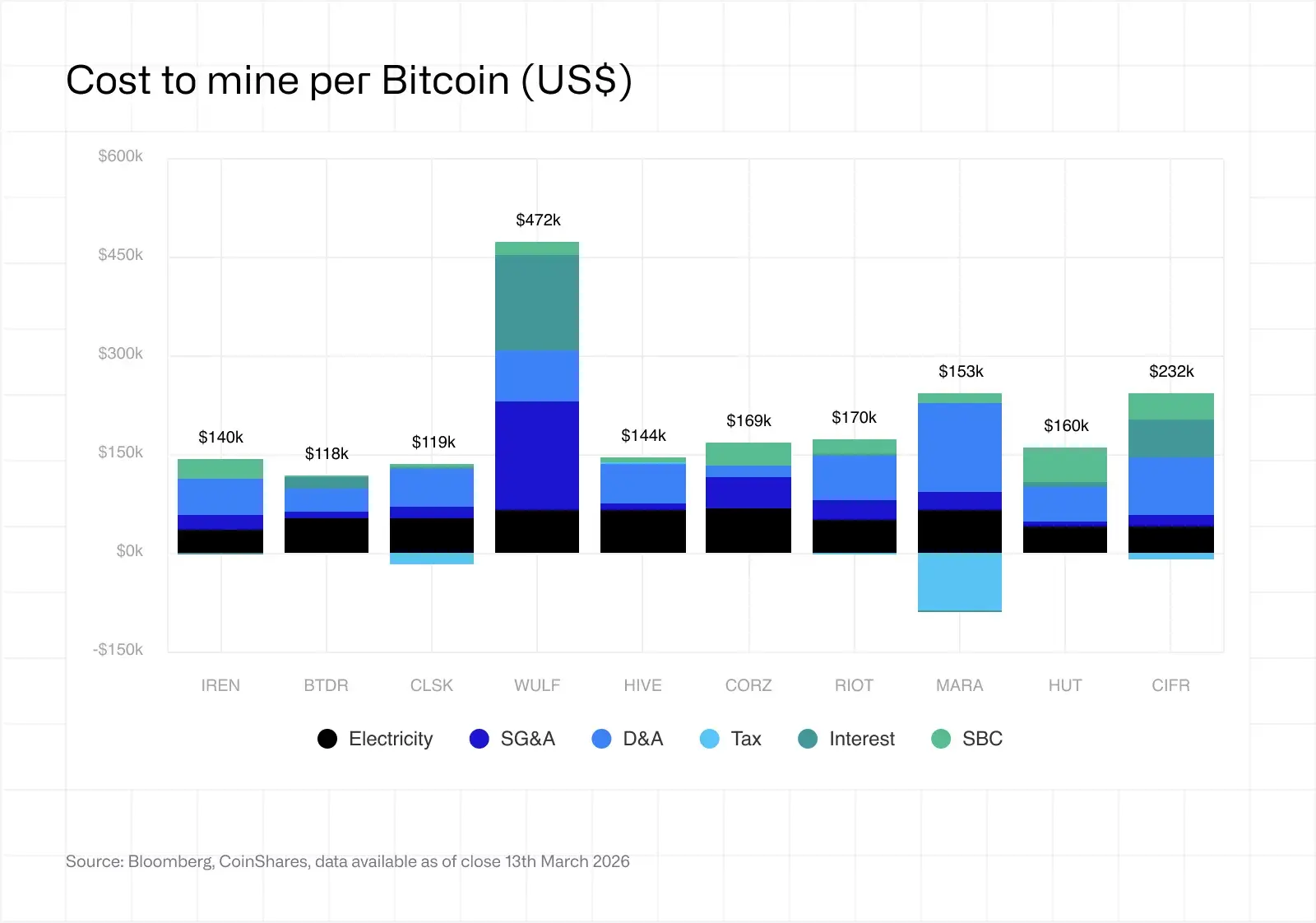

Cost to Mine Analysis Reveals Widening Dispersion between AI-Pivoting and Pure-Play Operators

The weighted average cash cost to produce one Bitcoin among publicly listed miners rose to approximately $79,995 in Q4 2025, with significant dispersion between operators. CleanSpark reported an all-in cost of $118,932 per BTC with cash costs of $71,188, reflecting operational discipline, minimal leverage, and fleet efficiency of approximately 16 W/TH. Bitdeer reported an all-in cost of $118,188 per BTC with cash costs of $87,144, though its proprietary ASIC strategy and multi-segment revenue structure complicate US GAAP peer comparisons.

(Source: CoinShares, Bloomberg)

Marathon Holdings reported an all-in cost of $153,040 per BTC with cash costs of $103,605, distorted by a $183.4 million income tax benefit driven by fair value adjustments on BTC holdings. Excluding this non-operational benefit, the all-in cost rises to $240,407. Riot Platforms reported an all-in cost of $170,366 per BTC with cash costs of $102,538, benefiting from $9.9 million in Q4 ERCOT demand response credits.

AI-pivoting operators show cost-per-BTC metrics that are not comparable to pure-play peers. TeraWulf reported an all-in cost of $471,841 per BTC, reflecting interest costs of $144,974 per BTC on $5.7 billion in total debt, SG&A of $167,221 per BTC, and D&A of $77,217 per BTC as the company transitions to an AI/HPC infrastructure business. Cipher Digital reported an all-in cost of $231,980 per BTC, driven by D&A of $87,768 per BTC under a three-year useful life assumption and interest of $56,445 per BTC following $1.733 billion in senior secured notes issued in November 2025.

Hut 8 reported an all-in cost of $160,402 per BTC with cash costs of $50,332, though the headline cost is influenced by $48,527 per BTC in stock-based compensation from CEO and CSO equity grants and a $17.8 million Canadian HST refund that lowered G&A. HIVE Digital reported an all-in cost of $144,321 per BTC with cash costs of $75,274, carrying just $13.8 million in total debt—the lowest leverage in the peer group—while facing a contingent VAT liability of approximately $79.2 million from Swedish Tax Agency assessments.

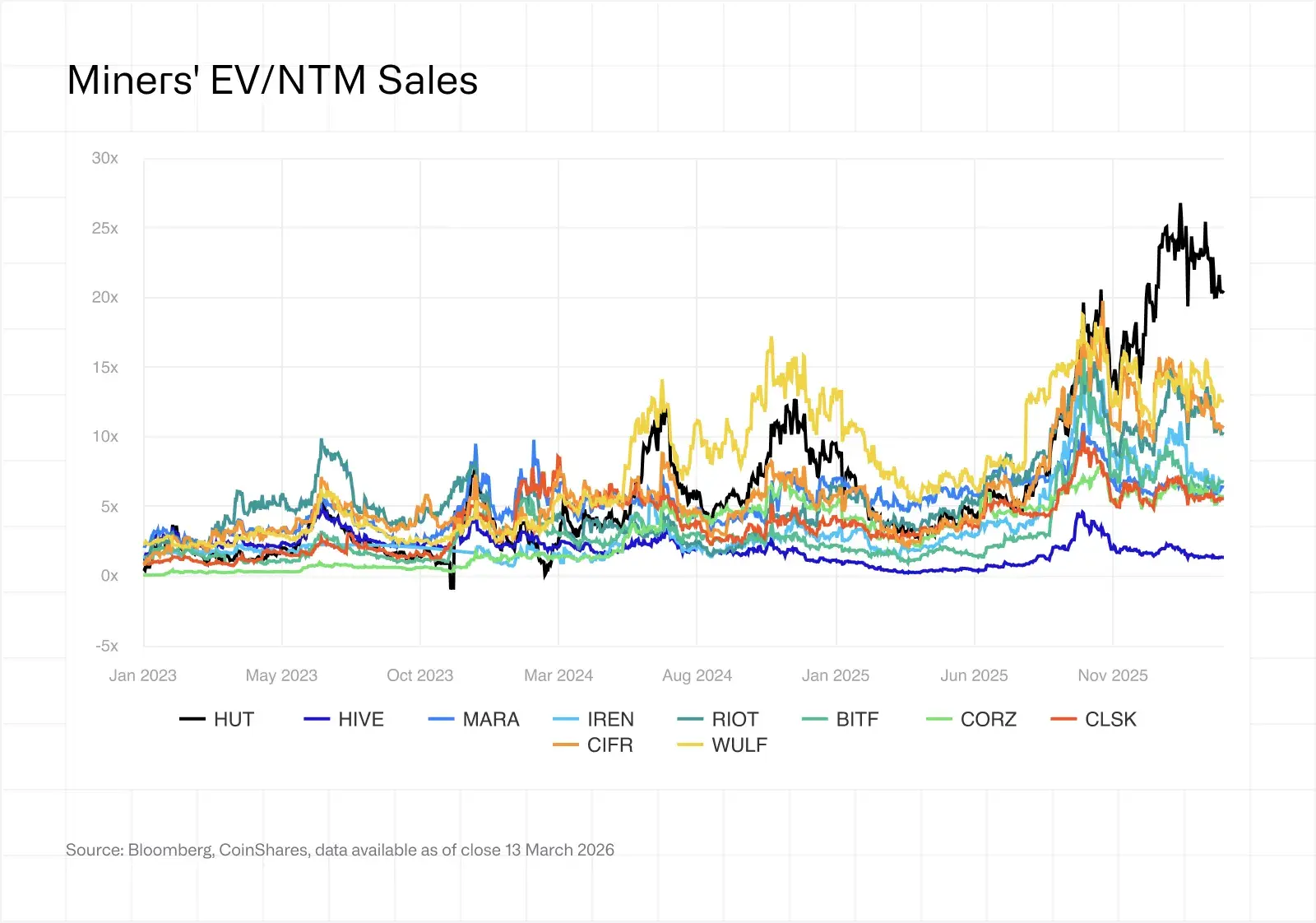

Miner Stock Performance Bifurcates between AI Infrastructure and Pure-Play Mining

The AI/HPC valuation premium continued to widen in Q4 2025 and Q1 2026. Miners with secured HPC contracts now trade at EV/NTM sales multiples of approximately 12.3x, while pure-play miners trade at 5.9x. The sector has fundamentally bifurcated into infrastructure companies—including TeraWulf, Core Scientific, Cipher Digital, and Hut 8—and mining companies—including Marathon Holdings, CleanSpark, Riot Platforms, and HIVE Digital.

(Source: CoinShares)

Short interest remains elevated across the sector, with Marathon Holdings at approximately 30% of float. The Q4 BTC price decline of 31% from its all-time high created a double headwind of lower mining revenue and reduced value of BTC treasury holdings. Whether AI-focused multiples are justified depends on execution, as not all announced deals will translate to operational infrastructure and capital requirements remain substantial.

Outlook for 2026 Centers on Hash Price Recovery, AI Revenue Inflection, and Consolidation

Hash price recovery remains contingent on BTC price. At approximately $70,000 BTC and $30 hash price, many mid-generation fleets are at or below breakeven. A sustained move below $70,000 could trigger larger capitulation, paradoxically benefiting survivors through lower difficulty. Next-generation hardware deployment, including Bitmain S23 series and SEALMINER A3 with sub-10 J/TH efficiency, is expected at scale through H1 2026, widening the efficiency gap and accelerating fleet refresh cycles.

AI and HPC revenue inflection will be closely watched as Core Scientific targets full 590MW CoreWeave delivery by early 2027 and TeraWulf continues its Lake Mariner buildout. The market will monitor whether contracted revenue converts to billings and whether margins reach 85%+ targets. Dispersion in leverage may create M&A catalysts, with miners holding clean balance sheets and strong liquidity positions, such as HIVE and CleanSpark, potentially acting as acquirers.

Geographic and regulatory shifts continue to shape the sector. The United States continues gaining market share, while Paraguay and Ethiopia emerge as mining geographies. Texas SB 6, signed in June 2025, imposed new requirements on large mining and data center loads connecting to ERCOT, including mandatory remote disconnection capability. Consolidation is expected to continue in 2026, with the efficiency gap between best-in-class fleets at approximately 15 W/TH and lagging fleets above 25 W/TH wide enough that acquiring efficient capacity may be cheaper than upgrading legacy operations.

FAQ

What drove Bitcoin miners to pivot toward AI infrastructure in 2025 and 2026?

Hash price declined from $63/PH/s in July 2025 to $29/PH/s in March 2026, compressing mining margins, while AI infrastructure offers structurally higher and more stable returns. Publicly listed miners have announced over $70 billion in cumulative AI and HPC contracts, with several operators targeting 70% of revenue from AI by the end of 2026.

How did network hashrate and mining economics change in Q1 2026?

Network hashrate recovered to approximately 1,020 EH/s after declining 10% from its October 2025 peak of 1,160 EH/s. Hash price fell to $29/PH/s, pressuring mid-generation hardware such as S19j Pro-class miners at average industrial electricity costs of $0.05/kWh. Approximately 15–20% of the global mining fleet is estimated to be unprofitable at current prices.

Which Bitcoin miners have the lowest all-in production costs?

CleanSpark reported an all-in cost of $118,932 per BTC with cash costs of $71,188, reflecting operational discipline and minimal leverage. Bitdeer reported $118,188 per BTC with cash costs of $87,144, benefiting from proprietary ASIC manufacturing. Both operators maintain fleet efficiency at approximately 16 W/TH, significantly better than the 25+ W/TH of lagging fleets.