Many people ask, “What is X Money?” and often equate it with a simple transfer feature within X. That’s an incomplete picture. More precisely, X Money is a financial infrastructure layer built by the X platform, designed to create a seamless ecosystem connecting content, social interactions, creator engagement, and commercial transactions.

From a product standpoint, X Money might appear as a wallet, a transfer gateway, or a withdrawal option. But beneath the surface, it consists of an account system, funding channels, risk control strategies, settlement capabilities, and a compliance framework. In short, X Money isn’t a single feature—it’s the foundational transaction layer that X must have to evolve into a super app.

Latest Updates: From Strategic Partnerships to External Beta

Drawing on recent public disclosures, X Money’s development can be summarized as “partnerships first, licensing progress, and product pilots.” The market is currently focused on several key milestones:

-

X has established a payment partnership with Visa, enhancing the potential for external funding access and transfer capabilities.

-

X has repeatedly communicated expected timelines for the external Beta release of X Money, showing that it’s moved beyond just a roadmap concept.

-

Payment licenses are advancing under the logic of U.S. state-level regulation, with compliance progress varying by state.

In other words, X Money has entered the “validation stage”—the question is no longer if it will launch, but where it will roll out first, to what extent, and whether it can scale reliably.

What X Money Can—and Can’t—Do

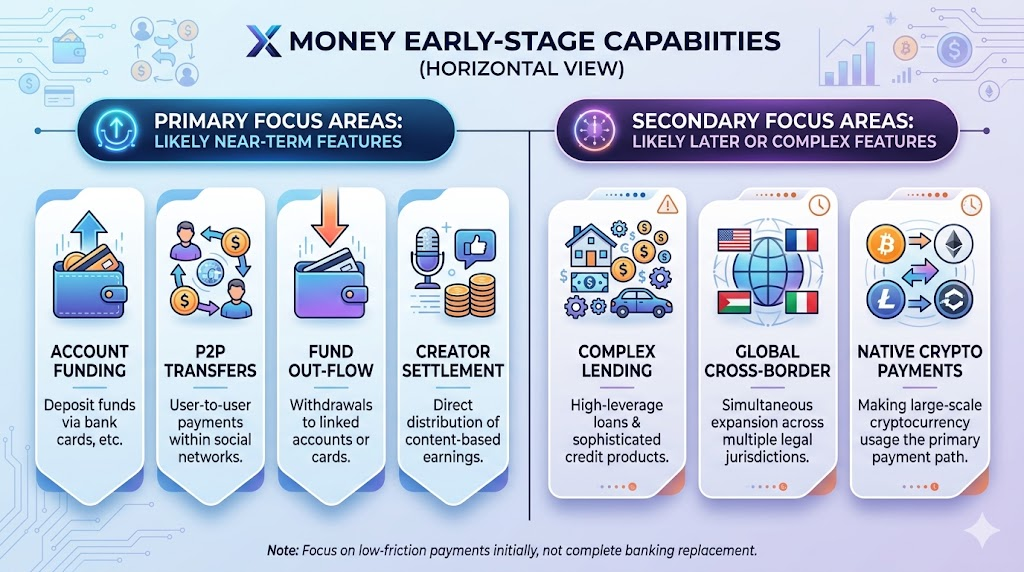

Based on public statements and typical industry rollouts, X Money’s early features will likely focus on “low friction, low complexity” payments rather than offering a full suite of financial services from day one.

Capabilities likely to launch first:

-

Account deposits: Add funds to your wallet using a bank card or similar methods.

-

Peer-to-peer transfers: P2P payments within your social network.

-

Fund withdrawals: Withdraw funds to a linked account or card.

-

Creator settlements: More closely connect content engagement with revenue distribution.

Capabilities unlikely to be aggressively pursued in the short term:

-

Complex credit products and high leverage financial features.

-

Simultaneous cross-border, multi-jurisdictional launches.

-

Large-scale crypto asset payments as the primary channel.

For most users, this phase is about “integrating payments into the social platform”—not “replacing all banking services with a new platform.”

Why Visa? The Power of Settlement Networks and Trust

Global card networks like Visa play a crucial role in X Money’s early rollout.

Network capabilities. The biggest challenges in payments aren’t the front-end buttons—they’re the back-end settlement, fund availability, failed transaction retries, and exception handling. Partnering with an established network dramatically reduces system complexity.

Trust transfer. Whether users are willing to store funds in a new wallet depends on whether their money is safe, withdrawable, and traceable. Having a trusted payment network involved provides critical initial trust.

Compliance alignment. While partnerships don’t replace licensing, established institutions offer proven templates for fraud prevention, transaction monitoring, and dispute resolution, helping X avoid costly mistakes.

Regulation and Licensing: The Ceiling for X Money

A key reality in payments: no matter how good the product experience is, without a strong regulatory foundation, scale will hit a wall. This is the core challenge facing X Money.

U.S. payment licenses differ significantly by state, so progress won’t be uniform. For X Money, licensing status directly impacts three areas:

-

Whether real fund flows can be enabled at scale.

-

Whether a full deposit-transfer-withdrawal cycle can be offered.

-

Whether merchants, creators, and users can expect stable, ongoing service.

Regulators also focus on more than just license count—they look at ongoing compliance: KYC, AML, suspicious transaction monitoring, account freezing and appeals, and data governance. Building these capabilities takes time and organizational commitment—it’s not something a single product launch can solve.

How X Money Differs from WeChat Pay, PayPal, and Cash App

Discussions about X Money often reference WeChat Pay, PayPal, and Cash App. These comparisons are useful, but it’s a mistake to think “feature parity equals competitive parity.”

-

WeChat Pay’s strength is deep integration with high-frequency daily life and merchant networks.

-

PayPal’s advantage is its cross-border payment history and merchant ecosystem.

-

Cash App stands out for its popularity with younger users and easy personal finance access.

-

X Money’s potential edge is embedding payments into real-time content and social interactions.

In other words, X Money’s breakthrough may not be “being a better wallet”—it may be “making payments a seamless part of social interaction.” If successful, it creates a new transaction entry point; if not, it’s just another wallet.

The Top 5 User Concerns

These are the most common—and most influential—questions affecting X Money adoption:

Is my money safe?

- Users care most about whether lost funds can be recovered—not just marketing promises.

Are payments fast?

- Certainty is key for P2P payments: how long does it take, and what happens if it fails?

Are fees high?

- Low fees drive trial; high transparency drives long-term retention.

How is privacy and data segregation handled?

- Separating social and payment data is crucial for building trust.

Is customer support and dispute resolution available?

- In reality, reputation is built on how well exceptions are handled.

Industry experience shows that payment products succeed or fail not on “can you transfer,” but on “can you handle exceptions reliably.”

From a platform strategy perspective, X is building X Money for three core reasons:

-

Boost transaction conversion: Link content consumption, tipping, subscriptions, and service purchases directly to payments.

-

Increase user stickiness: Once users have funds on the platform, switching costs rise dramatically.

-

Diversify revenue streams: Compared to ads alone, payments and financial services offer more stable take rate opportunities.

This is why “What is X Money?” can’t be answered just from a product perspective—it’s a platform-level competition issue. It will determine whether X can evolve from an information platform into a true transaction platform.