After the tide recedes: Which Web3 projects are still making money?

What is the survival baseline for crypto projects after the bubble has burst?

Back when every story sold and sky-high valuations were the norm, cash flow felt optional. That’s no longer the case.

Venture capital is retreating, and liquidity is drying up. In this market, the ability to generate real profits and maintain positive cash flow is now the first test of a project’s fundamentals.

Meanwhile, some projects are riding out the cycles with consistent revenue. According to DeFiLlama, in October 2025, the top three crypto projects by revenue—Tether, Circle, and Hyperliquid—each brought in $688 million, $237 million, and $102 million in monthly revenue, respectively.

This article explores these projects with genuine cash flow. Most revolve around two core drivers: trading and attention. These are the two most fundamental sources of value in business, and crypto is no exception.

Centralized Exchanges: The Steadiest Revenue Model

It’s no secret in crypto that exchanges are the most profitable businesses around.

Exchanges primarily earn through trading fees and listing fees. Take Binance: its spot and derivatives volumes have long accounted for 30–40% of the entire market. Even in the bleakest markets of 2022, it posted $12 billion in annual revenue—and in bull cycles, that number only grows. (Data: CryptoQuant)

Simply put: as long as trading happens, exchanges make money.

Coinbase offers another example. As a public company, its disclosures are clear: in Q3 2025, Coinbase reported $1.9 billion in revenue and $433 million in net profit. Trading is the primary driver, accounting for over half, with the remainder from subscriptions and services. Other major players like Kraken and OKX are also posting solid profits—Kraken reportedly earned about $1.5 billion in 2024.

The key advantage for CEXs is inherent: trading activity directly generates revenue. Unlike many projects still struggling to prove their business models, CEXs are already collecting real service fees.

In short, as storytelling gets tougher and hot money dries up, CEXs are among the few players that can survive on their own, without outside funding.

On-Chain Projects: PerpDexes, Stablecoins, and Public Chains

According to DefiLlama (as of November 27, 2025), the top ten on-chain protocols by revenue over the past 30 days are shown below.

Clearly, Tether and Circle dominate the top spots. Thanks to the US Treasury yield spread behind USDT and USDC, these two stablecoin issuers rake in nearly $1 billion a month. Hyperliquid follows as the most profitable on-chain derivatives protocol. The rapid rise of projects like Pumpfun again proves the old adage: “It’s better to sell coins than trade them, and better to sell tools than shovels”—a logic that still holds in crypto.

Notably, up-and-comers like Axiom Pro and Lighter, though smaller in scale, have already found a path to positive cash flow.

PerpDex: Real Revenue for On-Chain Protocols

This year, Hyperliquid has been the standout PerpDex.

Hyperliquid is a decentralized perpetuals platform with its own independent chain and matching engine. Its surge was dramatic: in August 2025 alone, it processed $383 billion in trading volume and earned $106 million in revenue. The platform allocates 32% of revenue to buy back and burn its native tokens. As reported by @wublockchain12 yesterday, the Hyperliquid team unlocked 1.75 million HYPE ($60.4 million), with no outside funding or sell pressure, and protocol revenue used for buybacks.

For an on-chain project, this rivals the revenue efficiency of CEXs. More importantly, Hyperliquid is truly generating profits and feeding them back into its token economy—creating a direct link between protocol revenue and token value.

Now, consider Uniswap.

For years, Uniswap faced criticism for “freeloading” token holders: it charged a 0.3% fee per trade, all of which went to LPs, while UNI holders received nothing.

In November 2025, Uniswap announced plans to launch a protocol fee-sharing mechanism and use some historical revenue to buy back and burn UNI tokens. Estimates suggest that if this had been implemented earlier, $150 million could have been used for token burns in just the first ten months of the year. The news sent UNI soaring 40% in a single day. While Uniswap’s market share has slipped from a 60% peak to 15%, this proposal could still reshape UNI’s fundamentals. However, after the announcement, @EmberCN observed a UNI investor (possibly Variant Fund) moving millions of $UNI ($27.08 million) into Coinbase Prime—likely to sell into strength.

All told, the old DEX model of airdrop-fueled speculation is running out of road. Only projects that achieve stable, closed-loop revenue can truly retain users.

Stablecoins and Public Chains: Passive Income from Interest

Beyond trading, infrastructure projects like stablecoin issuers and high-traffic public chains continue to pull in capital.

Tether: The Relentless Money Printer

Tether, the company behind USDT, runs a straightforward business: for every $1 deposited to mint USDT, Tether invests it in Treasuries, commercial paper, and other low-risk, interest-bearing assets, pocketing the interest. As global rates rose, Tether’s profits soared—$13.4 billion in net profit for 2024, and a projected $15 billion in 2025, putting it close to traditional giants like Goldman Sachs. @Phyrex_Ni recently noted that despite a ratings downgrade, Tether remains a cash cow, passively earning over $130 billion in collateral from US Treasuries.

Circle, which issues USDC, has slightly less circulation and profit, but still brought in over $1.6 billion in 2024, with 99% from interest income. Circle’s profit margins aren’t as high as Tether’s, partly due to revenue sharing with Coinbase. In essence, stablecoin issuers are money printers—they don’t need to spin stories or raise funds, just rely on users’ willingness to deposit. In bear markets, these savings-focused projects actually thrive. @BTCdayu also calls stablecoins a great business—earning global interest, with Circle as the king of passive stablecoin income.

Public Chains: Earning from Usage, Not Incentives

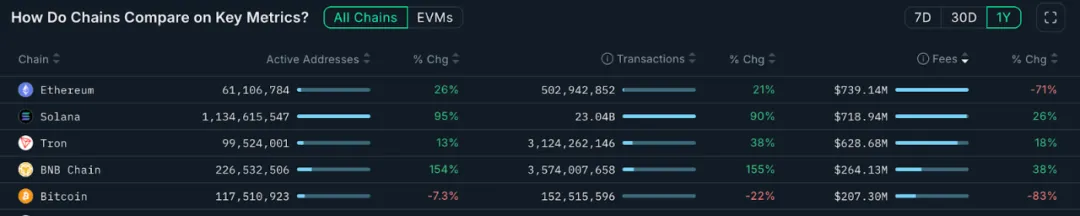

Mainnet public chains monetize most directly through gas fees. The chart below is from Nansen.ai:

Over the past year, transaction fee revenue shows which chains have real usage value. Ethereum brought in $739 million, still the leader, but down 71% year-over-year due to the Dencun upgrade and L2 migration. Solana, by contrast, earned $719 million—a 26% annual increase—driven by surging activity around memes and AI Agents. Tron netted $628 million, up 18%. Bitcoin’s $207 million was down sharply as inscription trading cooled.

BNB Chain earned $264 million for the year, up 38%, leading mainstream public chains in growth. While its revenue still lags behind ETH, SOL, and TRX, its growing transaction volume and active addresses signal expanding use cases and a more diverse user base. BNB Chain’s steady growth supports its evolving ecosystem.

Public chains are the “water sellers”—no matter who’s digging for gold, everyone needs their water, electricity, and roads. These infrastructure projects may lack short-term hype, but they deliver stability and resilience across cycles.

KOL-Driven Businesses: Monetizing Attention

If trading and infrastructure are the obvious business models, the attention economy is crypto’s “hidden game”—think KOLs and agencies.

This year, crypto KOLs have become the center of attention and traffic.

Leading influencers on X, Telegram, and YouTube leverage their reach for diversified revenue—paid promotions, community subscriptions, monetized courses, and more. Industry chatter says mid-tier and above KOLs can earn $10,000 a month from promotions alone. As audiences demand higher-quality content, only KOLs who win user trust through expertise, judgment, or deep engagement can survive the cycles. This trend is reshaping the content landscape: the impatient exit, while long-term players endure.

There’s also a third layer of attention monetization: KOL fundraising rounds. Here, KOLs become primary market players, acquiring project tokens at a discount in exchange for exposure—early-stage “influence chips” that bypass VCs entirely.

An entire matchmaking ecosystem has emerged around KOLs, with agencies acting as traffic brokers—matching projects to the right influencers. The whole pipeline is starting to resemble a sophisticated ad system. For more on these KOL and agency models, see our long-form piece, “Inside the KOL Round: A Wealth Experiment Driven by Traffic” (https://x.com/BiteyeCN/status/1986748741592711374), for a deep dive into the real economics at play.

Ultimately, the attention economy is about monetizing trust. In a bear market, trust is even more scarce—and the bar for monetization is even higher.

Conclusion

Projects that maintain cash flow through the crypto winter all prove one thing: trading and attention are the industry’s bedrock.

On one hand, whether centralized or decentralized, trading platforms with robust user activity can generate steady revenue from fees. This direct business model lets them stay self-sufficient even as capital retreats. On the other hand, KOLs focused on user attention monetize value through ads and services.

We may see more diverse models in the future, but projects that build real revenue during market downturns will be best positioned to lead the next phase. By contrast, those that rely solely on storytelling and lack genuine revenue—even if they see short-term hype—are likely to fade away.

Statement:

- This article is reproduced from [Biteye], with copyright belonging to the original author [Viee]. For any concerns regarding republication, please contact the Gate Learn team for prompt handling according to relevant procedures.

- Disclaimer: The views and opinions expressed herein are those of the author and do not constitute investment advice.

- Other language versions are translated by the Gate Learn team. Without mention of Gate, reproduction, distribution, or plagiarism of the translated article is prohibited.

Share

Content

Related Articles

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Solana Need L2s And Appchains?

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?